Circle of Competence: I Almost Bought NVIDIA Because I Like Data Centers

The $4.5 billion question I couldn’t answer and what it taught me about the gap between liking an industry and understanding an investment.

A few weeks ago I had NVIDIA’s earnings report open in one tab and my brokerage account open in another.

The numbers were absurd. Revenue up 85% in a single quarter. Data center revenue nearly doubling year over year. And I sat there thinking the sentence that almost every beginner thinks at some point:

I work in infrastructure. I understand servers, networks, data centers, why AI needs all this compute. This is my area. I should own this.

I didn’t buy. Not because I’m disciplined, still working on this, but because I made myself try to actually explain the investment before clicking the button, and I couldn’t. Halfway through writing down why NVIDIA was a good buy at today’s price, I realized I was writing down why NVIDIA is an impressive company. Those are not the same sentence, and the gap between them is the entire subject of this post.

This is me learning in public, so I’ll show you exactly where my reasoning fell apart, what I looked up, the one number that scared me until I read one paragraph of a filing, and the rule I’m using now.

What “circle of competence” actually means (and the part everyone skips)

The phrase comes from Warren Buffett: invest inside the set of businesses you can actually understand, and be honest about where that set ends.

Everyone quotes the first half. The useful half is “be honest about where it ends”. The circle isn’t a list of industries you find interesting. It’s the much smaller set of businesses where you can answer, without hand-waving: what does this company sell, why do customers pay for it instead of the alternative, what is the moat if any, what could break that, and this is the one beginners drop at what price does the stock stop being worth it?

Here’s the trap I walked straight into. There are three completely different claims hiding inside “I understand semiconductors”:

- I like the technology. (True. I genuinely enjoy this stuff extensively)

- I understand the business. (Sometimes. Less than I think, work in progress)

- I know whether the stock is a good buy at today’s price. (Almost never, yet)

I had quietly let the first one stand in for the third. Liking GPUs is not a thesis. It’s a reason to start reading. It is not permission to buy.

The test I gave myself: can I actually analyze NVIDIA?

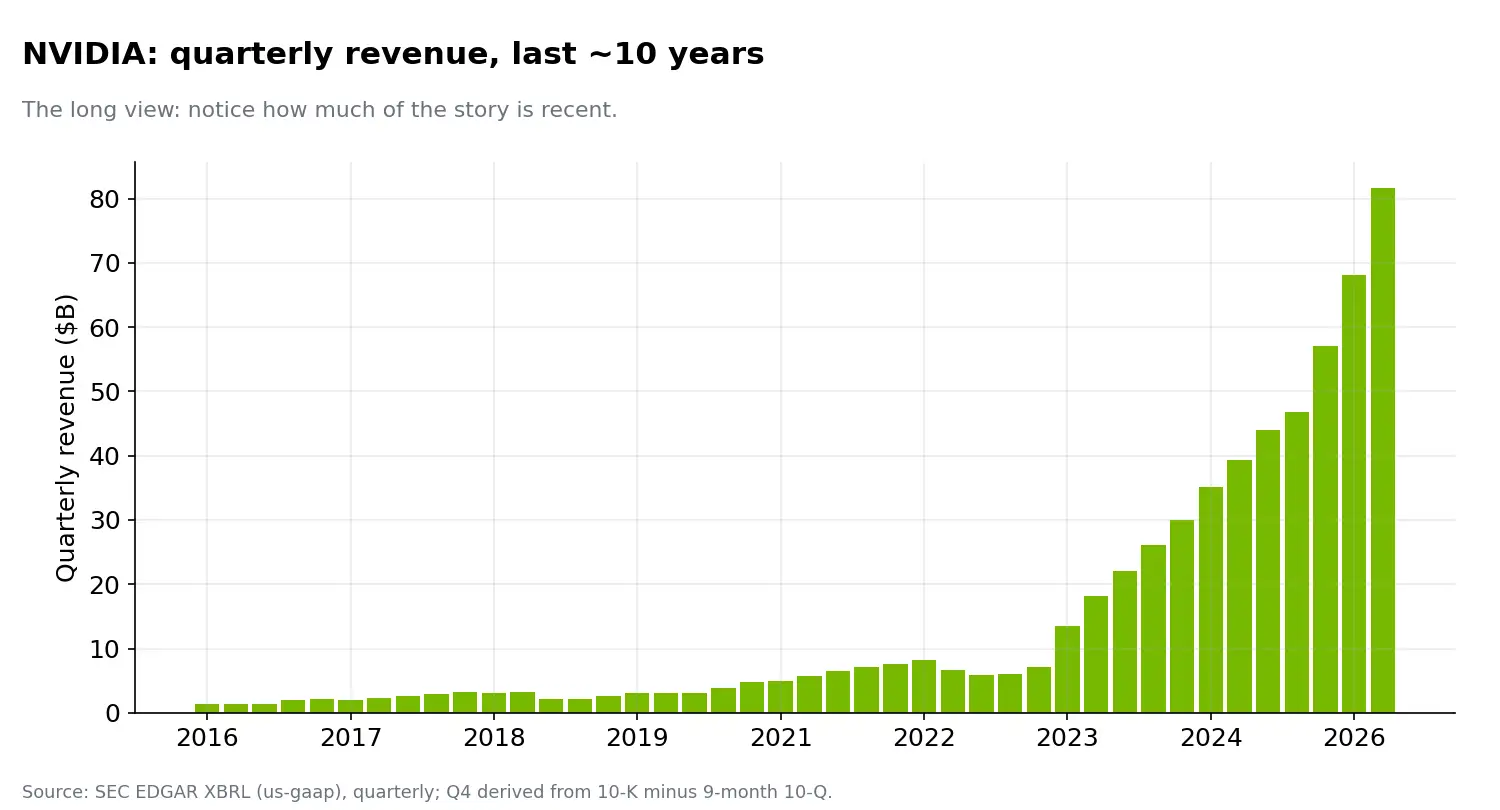

Let me show you the real numbers, because they matter for what comes next. These are from NVIDIA’s actual filings, not vibes:

- Fiscal 2026 (ended January 2026): revenue of $215.938 billion, up 65%, with data center revenue of $193.7 billion, up 68%.

- Then in the quarter reported on May 20, 2026: revenue of * $81.615 billion, up 85% year over year, with data center revenue of $75.246 billion, up 92%*.

Astonishing. And here’s where a beginner me, a few weeks ago reads those numbers and concludes “this proves it’s a great investment.” It doesn’t. It proves the business has been great recently. It says nothing on its own about whether the stock gives me a good return from the price I’d pay today. Those are different questions, and the market has already seen these results too.

So I tried to do real analysis. I got through about two questions before I hit a wall.

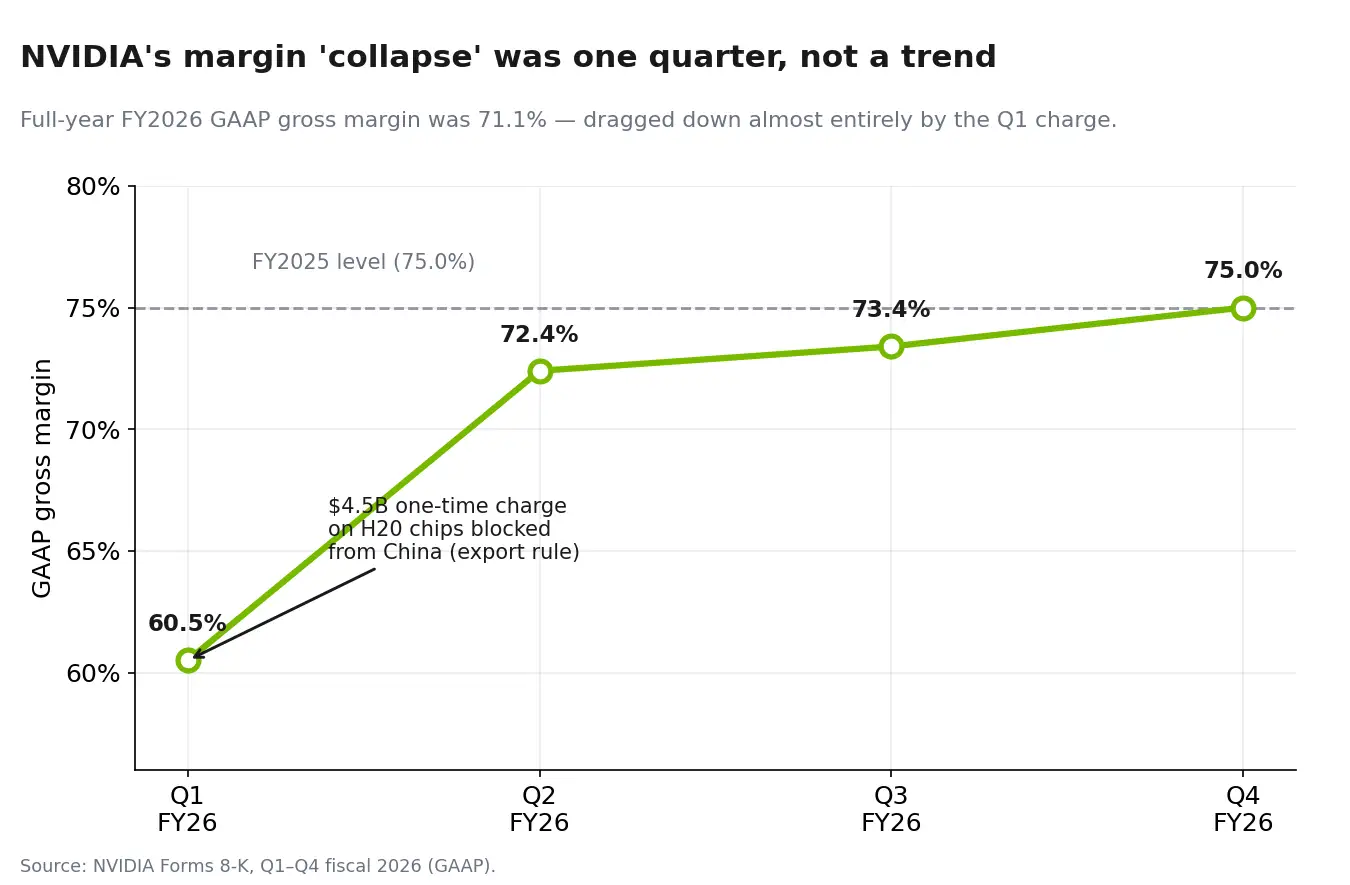

The number that scared me, and the lesson in it. I noticed NVIDIA’s full-year GAAP gross margin fell, from around 75% in fiscal 2025 to 71.1% in fiscal 2026. My gut reaction was the dramatic one: margins are compressing, competition is biting, the moat is cracking. That’s exactly the kind of “red flag” a nervous beginner latches onto.

Then I did the thing I’m supposed to do I read the filing instead of trusting my gut. The drop was driven mostly by a $4.5 billion one-time charge in the first quarter tied to H20 chips it couldn’t sell into China after new U.S. export rules. It wasn’t pricing power eroding. And by the fourth quarter of that same year, gross margin was already back to 75%.

I was wrong about what the number meant, and finding out took one search. That’s the actual lesson of this whole post in miniature: a number that looks like a warning can dissolve the second you read one paragraph and you only find out if you do the work instead of reacting to the surface. I almost let a scary-looking chart talk me out of a company for the wrong reason, the same way I’d almost let a great-looking chart talk me into it.

Where I genuinely tapped out. Past the margin question, the real ones started, and these I could not answer honestly:

- Why does a customer keep buying NVIDIA instead of a cheaper alternative or its own custom chip? (I can say “the software ecosystem and the full system, not just the chip”, but I can’t size how durable that is.)

- The biggest customers are a handful of giant cloud companies. Those same giants are the most capable of, and most motivated to, build their own alternatives. How much does that threaten NVIDIA, and when?

- How much of this insane demand is a one-time scramble for capacity, and how much is durable?

And the question that ends the discussion: can I value it?

Let me show you what even a crude attempt looks like, because I spent the whole first draft of this post telling you valuation matters and never once showing it. Here’s the back-of-the-envelope version anyone can do:

NVIDIA earned roughly $120 billion in net income in fiscal 2026. Go pull up its current market value (do this yourself, prices move). Divide market value by that ~$ 120 billion and you get a price-to-earnings multiple. When I checked, paying for NVIDIA meant paying somewhere in the low-to-mid 30s times earnings. That’s not a verdict, it’s a question generator. Paying ~33× earnings only makes sense if profits keep growing fast for years. So the real question becomes: what happens to that multiple if data center growth slows from 90% to, say, 30%? The business could still be wonderful and the stock could still fall, because the price already assumes wonderful.

I don’t have a confident answer to that. Which means NVIDIA is, for me, today, a study not a buy. Not forever. Just until I can finish that paragraph without hiding behind “AI is the future”.

So I moved to a company closer to my actual circle: Arista

Here’s where being honest about the edge of the circle is more useful than pretending the whole thing is inside it.

I worked close to networking and infrastructure. A data center isn’t just a warehouse of CPUs and GPUs those chips have to talk to each other at enormous speed, and the network is where things bottleneck. That’s a problem I actually recognize from real work. So Arista Networks is a far more sensible first deep-dive for me than, say, ASML, whose business sits inside lithography physics I’d have to learn from scratch.

The two-sentence version I could write without faking it: Arista sells high-performance switches and, more importantly, the software (its EOS operating system) that runs large cloud and AI networks. Its pitch is replacing closed, proprietary gear with something more open and easier for hyperscalers to operate at scale.

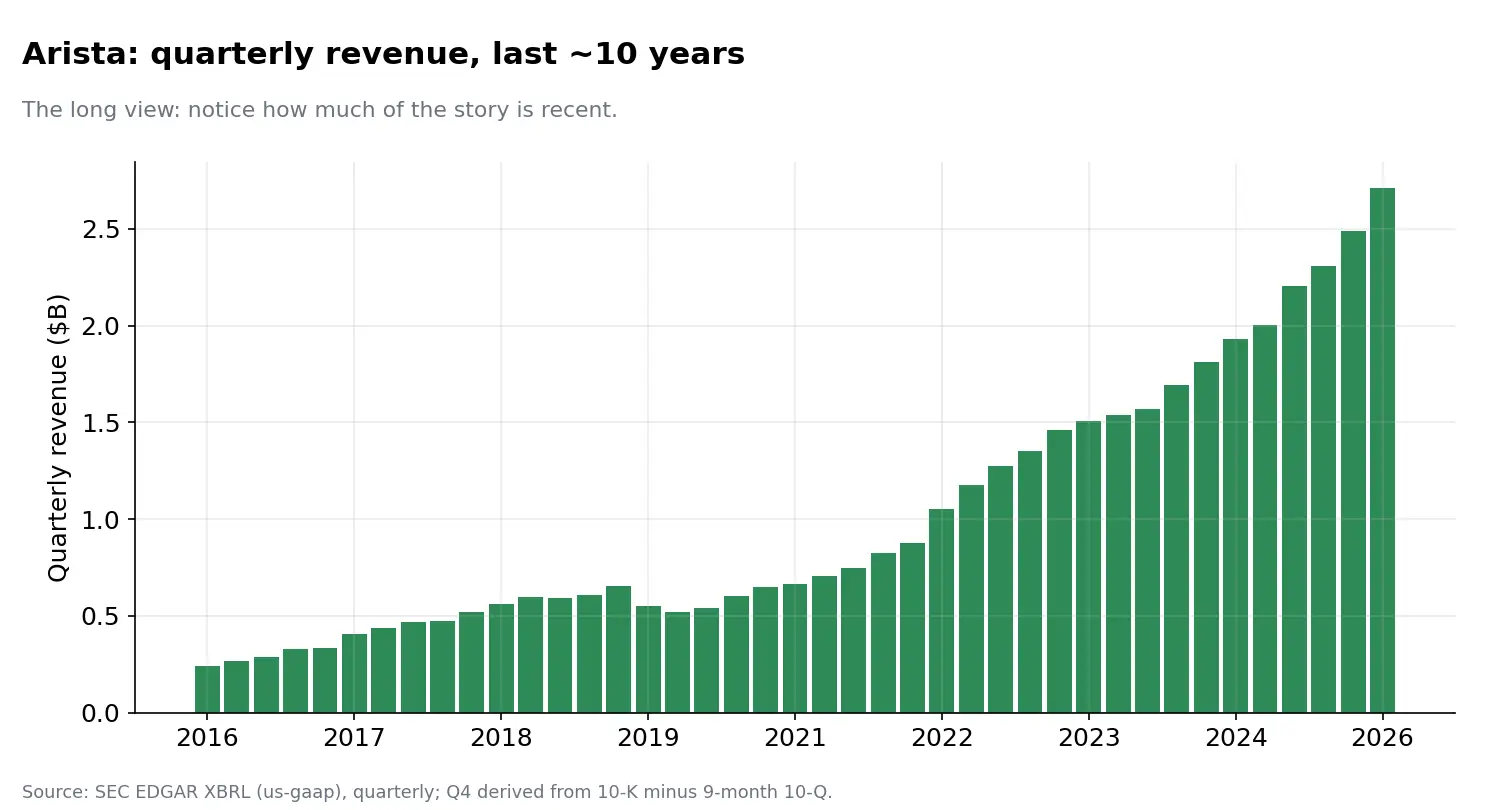

The numbers, again real ones: in 2025 Arista did * $9.006 billion in revenue, up 28.6%, kept a 64.1% gross margin, and grew GAAP net income to $3.511 billion* from $2.852 billion. A company genuinely riding AI-networking demand while staying very profitable.

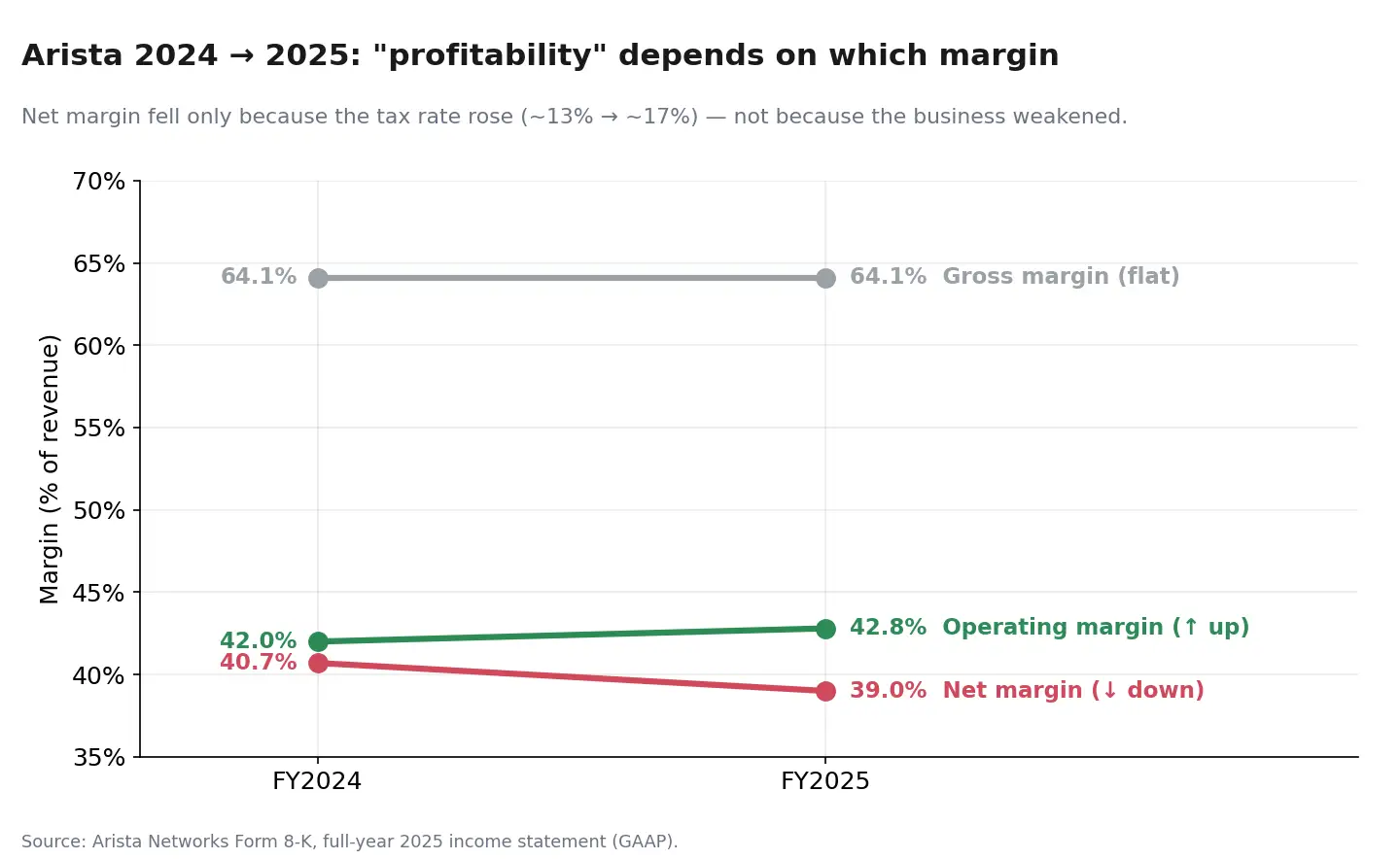

Here’s the discipline test passing and a second trap I nearly walked into, different from the NVIDIA one. Writing this up, I almost added a worried line about Arista’s margins, because net margin slipped from about 40.7% in 2024 to 39.0% in 2025. “Profitability is falling,” I started to type then made myself read down the actual income statement instead of stopping at one number.

It said the opposite. Gross margin held flat at 64.1%, and GAAP operating margin actually rose to 42.8% from 42.0% the business got more efficient per dollar of revenue, not less. The whole net-margin dip came from below the operating line: the effective tax rate jumped from roughly 13% to 17% (2024’s was unusually low, helped by tax benefits on stock awards), while other income actually grew. That’s tax normalization, not a weakening business. The lesson is its own small one: “profitability fell” means nothing until you say which margin and why. Gross, operating, and net can move in opposite directions in the same year, and the cause can sit in a tax line that has nothing to do with how good the company is. I’d have published a wrong worry if I’d trusted the headline number.

That still isn’t a buy, though. The real cracks I can see, even on home turf, are two:

- Customer concentration. Arista itself flags that a large slice of revenue comes from a very small number of huge cloud customers. If one of them diversifies away or shifts to building its own gear, revenue could drop hard and fast.

- The “fail condition.” My thesis breaks if hyperscalers move to cheap white-box hardware they assemble themselves, or if NVIDIA’s own networking platform bundles in enough value to make Arista’s switches optional. I can name those risks. I can’t yet weigh them.

So even Arista the thing closest to what I actually know comes out as “I can explain the business, I can’t yet defend the price.” That’s a more honest place to be than I was with that brokerage tab open.

Why “I like semiconductors” is too vague to be a plan

Here’s the part that reframed everything for me. “Semiconductors and AI infrastructure” isn’t one business. It’s a chain of completely different businesses with completely different economics and risks:

| Layer | What it does | Companies to study |

|---|---|---|

| Chip design | Designs GPUs, CPUs, custom accelerators | NVIDIA, AMD, Broadcom |

| Manufacturing | Actually fabricates advanced chips | TSMC |

| Manufacturing equipment | Makes the machines that make chips | ASML, Applied Materials, Lam Research |

| Servers & systems | Integrates it into machines you can buy | Dell, Super Micro, HPE |

| Networking | Connects the clusters | Arista, Cisco, NVIDIA |

| Power & cooling | Keeps it running | Vertiv, Schneider Electric, Eaton |

| Cloud | Buys and operates it all | Microsoft, Amazon, Alphabet, Meta, Oracle |

A networking company faces nothing like the risks of a lithography company. A cloud giant buying GPUs is a fundamentally different bet than the company designing them. So “I’ll buy the semiconductor winners” isn’t a strategy it’s seven different strategies wearing one coat. The competent move isn’t to understand the whole chain at once. It’s to pick one layer you’re closest to and actually go deep. For me that’s networking and infrastructure. That’s the honest shape of my circle and if you want to learn more, you should take an eye on semianalysis.

The mistake that’s easy to make (and the one edge I actually have)

The core trap is simple to state and hard to feel: a true story about an industry feels exactly like a true thesis about a stock.

“AI will keep growing”

“Cloud will expand”

“Everyone needs data centers.”

All probably true. All nearly useless as investment cases, because they don’t tell you which company keeps the profit, for how long, or what price already bakes that in. And if everyone already believes the story, the price of the obvious winners already reflects it. A great company bought at a price that requires perfection can still be a bad investment.

The other thing I had to swallow: I am not going to out-analyze the professionals covering these names. They’ve read the filings, mapped the customers, built the models. “I understand GPUs because I like building rigs” is not an edge against that. So what is my edge, realistically? It’s smaller and more boring than I wanted:

My edge is being willing to not buy what I can’t explain. That’s it. It won’t make me money on any single trade. But it stops me from owning ten companies I can’t follow, panic-selling a stock I never understood when it drops 30%, and confusing a rising chart with a reason. For a beginner, avoiding unforced errors is worth more than a hot pick.

My rule now

I won’t buy a company because I like its industry, use its products, or believe its technology matters. Before I buy anything in semis, AI, or data-center infrastructure, I have to be able to say in plain words, on one page how it makes money, why customers pick it, what would break it, which numbers I’ll watch, and what price assumption I’m accepting. And I start every name on a study list, not a buy list, beginning with the layer closest to what I actually know not the most exciting headline.

This doesn’t require perfect knowledge. Nobody has that. It requires enough that the decision is mine, not borrowed from a video, a thread, or a green candle. Borrowed conviction is worthless precisely when you need it the moment the price falls.

Your action step

Don’t go search “best AI stocks.” Do the opposite. Pick one industry you genuinely know something about from your real life or work, and write a one-page competence map:

- The slice of it you actually understand.

- The companies operating closest to that slice.

- What you honestly don’t understand yet.

- The single company you’ll study first.

- The evidence you need before you’d consider buying at minimum: three years of revenue/margin/cash-flow, a one-paragraph explanation of the moat, the top risks in the company’s own words, one/more competitor comparison, and a rough valuation sketch like the one I did above.

My own next step is concrete: read Arista’s latest annual and quarterly reports, write that one page, compare it to Cisco, and refuse to buy until I can explain the valuation case out loud. That’s slower than buying NVIDIA on a Tuesday. Good. When it’s my actual savings, slow is the point.

A quick gut-check before you buy anything in this space

- Can I explain what it sells in two sentences without saying “AI”?

- Do I know who its biggest customers are and whether too few of them matter too much?

- Do I know whether margins are rising, flat, or falling, and why?

- What specific event would prove my thesis wrong?

- Roughly what growth does today’s price already assume?

- Would I still want to own it if the chart had been flat for two years?

- Am I buying a business, or am I chasing a story?

If I can’t get through that list, it doesn’t go in the portfolio. It goes in the research folder. That’s not me being timid. That’s the difference between investing and gambling with extra steps.

Next up, if I do this right: “I Studied Arista Before Buying Here’s What I Understand and What Still Stops Me.” If I can’t write that one honestly, that tells me something too.

Appendix

1. Reproduce the NVIDIA and Arista 10-Year Revenue and Gross Margin Graphs with Python

View fetch_edgar_data_and_chart.py on GitHub

This script retrieves company-reported US-GAAP revenue and gross-profit facts from the SEC EDGAR XBRL Company Concept API, calculates quarterly GAAP gross margin, derives missing fourth-quarter values where necessary, exports the underlying data to CSV files and creates the long-term charts used in this article.

2. Reproduce the NVIDIA Margin Recovery and Arista Profitability Comparison Graphs with Python

View make_margin_charts.py on GitHub

This script creates the focused comparison graphics used in the article: NVIDIA’s fiscal 2026 quarterly GAAP gross-margin path and Arista Networks’ fiscal 2024 versus fiscal 2025 gross, operating and net margin comparison.

Disclaimer

The charts use company-reported GAAP figures obtained from SEC EDGAR filings or the SEC XBRL API. The scripts are provided so readers can inspect the calculations and reproduce the visuals. XBRL data can include repeated comparative facts, amended filings and reporting-tag changes, so important values should be checked against the original filings before being used in an investment decision.

These scripts are educational examples created as part of my investing learning process. They are not investment advice or a recommendation to buy or sell NVIDIA, Arista Networks or any other security.

Comments

0